Brand awareness, marketing budgets, data: 5 interesting stats to start your week

We arm you with all the numbers you need to tackle the week ahead.

Brand awareness is marketers’ key objective

Brand awareness is marketers’ key objective

Brand awareness is marketers’ key objective

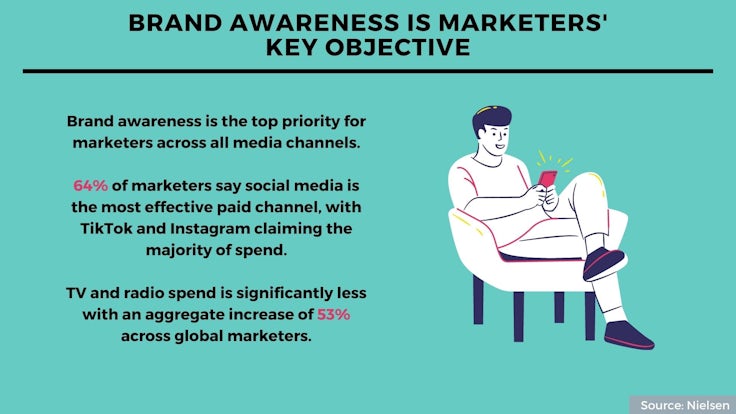

Brand awareness is marketers’ key objectiveBrand awareness is the top priority for marketers across all media channels, with customer acquisition cited as the second most-valued goal.

In their quest to increase awareness, almost two-thirds of marketers (64%) say social media is the most effective paid channel, with TikTok and Instagram claiming the majority of spend.

Comparatively, TV and radio spend is significantly less, with an aggregate increase of 53% across global marketers, according to the data from Nielsen’s Annual Marketing Report.

Given customer acquisition is brands’ second most important objective, the report suggests marketers must focus efforts on the entire customer journey.

Measurement is another big concern for marketers, but media fragmentation is making it harder to achieve. While 69% of marketers believe first-party data is essential for their strategies and campaigns, and 72% suggest they have access to quality data, just 26% of global marketers are fully confident in their audience data.

Marketers also lack confidence in their ability to measure return on investment, with only 53% confident in measuring full-funnel ROI. This drops below half across all other media once mobile video and online are removed from the equation. Podcasting is one area where marketers intend to invest more, however only 44% are confident in measuring the ROI of this channel.

Source: Nielsen

Average family saw discretionary income drop £52 in March

Households in the UK saw a fall in the amount of spare cash they had to spend last month. The average family saw their discretionary income drop by 4.9% in March 2022 compared to the same period last year, this amounted to £52 less to spend on things other than groceries and bills.

Households in the UK saw a fall in the amount of spare cash they had to spend last month. The average family saw their discretionary income drop by 4.9% in March 2022 compared to the same period last year, this amounted to £52 less to spend on things other than groceries and bills.

The cost of living crisis is being unevenly felt, with the least affluent seeing a far bigger portion of their discretionary spending being erased than the most affluent. The least affluent households saw their discretionary income drop by 5.2% in March 2022, compared to the year prior, equivalent to £26 less a month.

Meanwhile, the most affluent saw their discretionary income drop by £21 last month, £5 less in monetary terms than the least affluent. In terms of proportion of discretionary spending, this amounts to just 0.5% of the most affluent households’ spare cash.

These figures come from the Retail Economics-HyperJar Cost of Living Tracker, which finds that the loss in households’ discretionary spending is likely to have wiped out around £1.4bn worth of income for non-essentials throughout the month.

The research also finds that more than half (55%) of consumers see the rise in the cost of living as their biggest concern, followed by a weaker economy (13%), and lack of savings (8%).

Looking forward, consumers are worried about the ability to manage their spending. Around a quarter of consumers say they currently “just about manage” (25%) and nearly a third (30%) say that they are “a little concerned” about their current financial situation.

Source: Retail Economics-HyperJar

Brands up their marketing budgets as confidence grows in pandemic recovery

Marketing budgets have now been growing for four successive quarters, with a net balance of 14.1% of companies revising their marketing budgets upwards in the first quarter of 2022. This figure is the highest it has been for almost eight years.

Marketing budgets have now been growing for four successive quarters, with a net balance of 14.1% of companies revising their marketing budgets upwards in the first quarter of 2022. This figure is the highest it has been for almost eight years.

These figures come from the IPA Bellwether report on the first quarter of 2022. The figures represents a significant increase from the last quarter of 2022, when a net balance of 6.1% revised their marketing spend upwards.

Almost a quarter (24.1%) of surveyed companies upped their marketing spend in the first quarter of 2022, compared to just 10% which revised their budgets downward.

The increase in marketing spend reflects the UK’s emergence from the Covid-19 pandemic, and signifies more confidence among companies that they will be able to proceed without the disruption of lockdowns or restrictions.

However, the IPA warns the industry faces “strengthening headwinds” against its recovery, including inflation and the war in Ukraine.

The headwinds mean that slowed growth is expected in the coming months, which will negatively impact advertising spend. The IPA has revised down its growth figures to 3.5% in 2022 and 1.8% in 2023, from 5.2% and 2.5% respectively.

Source: IPA

Most British consumers see brands collecting data as ‘immoral’

British consumers want personalised experiences but are also sceptical of brands collecting their data. Around seven in 10 consumers say they see data collection by businesses as ‘immoral’. Consumers also say they’re growing more aware of how businesses use their data, with more than half (54%) saying they are more aware than in 2020.

British consumers want personalised experiences but are also sceptical of brands collecting their data. Around seven in 10 consumers say they see data collection by businesses as ‘immoral’. Consumers also say they’re growing more aware of how businesses use their data, with more than half (54%) saying they are more aware than in 2020.

Despite this, almost half of consumers didn’t realise that businesses sell their data to other companies.

Very few customers are aware of upcoming changes to third-party cookies, 80% reported they had no idea of the changes.

People are most aware of their online behaviour being used by brands but almost seven in 10 (67%) are uncomfortable with their internet history being used. The next most sensitive category is phone numbers, with 57% of users expressing discomfort with this companies knowing this information about them.

Despite scepticism around brands’ use of data, the research suggests that there is still an appetite for a more personalised experience. Less than one in five (16%) of consumers feel that the brands they interact with understand their needs as an individual.

Source: Rehab/YouGov

Shop sales slow as the cost of living crisis takes hold

Shop sales in the UK slowed last month as consumer confidence was dampened by concerns over inflation and the cost of living.

Shop sales in the UK slowed last month as consumer confidence was dampened by concerns over inflation and the cost of living.

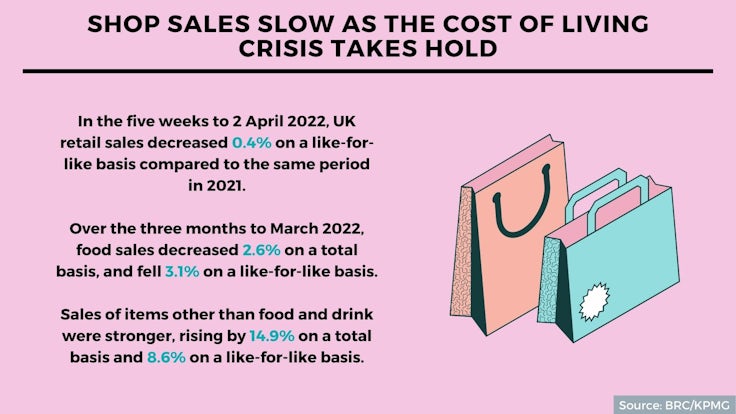

In the five weeks to 2 April 2022, UK retail sales decreased 0.4% on a like-for-like basis compared to the same period in 2021, when they increased 20.3%. The three-month average for growth was 3.2%, while the 12-month average growth was 6.5%.

Across food and non-food, total sales increased by 3.1% in March, compared to an increase of 13.9% in March 2021.

Food and drink sales particularly struggled over the period. Over the three months to March 2022, food sales decreased 2.6% on a total basis, and fell 3.1% on a like-for-like basis.

Sales of items other than food and drink were stronger, rising by 14.9% on a total basis and 8.6% on a like-for-like basis. This was driven in particular by in-store sales, which were up 92.9% on a total basis and 74.9% on a like-for-like basis, suggesting that consumers are returning to the high street.

Conversely, online sales on non-food dropped by 29% during March, having increased by 64.7% in the same month in 2021.

Source: BRC/KPMG